What is Commercial Banking, or Commercial Lending?

Commercial Lending is defined as the process of loaning money to businesses by banks or other financial services institutions. The process is much different than a loan made by commercial banks to individual consumers and is typically much more complex. Commercial loans can help businesses with mortgages for commercial real estate, short-term funding to float payroll, or even renewed indefinitely as a revolving line of credit based on incoming revenue. Most commercial loans are secured credit facilities backed up by collateral such as inventory, receivables, property, or even personal guarantee.

Commercial Lending is essential to all types of businesses, whether it is for funding long-term operational needs or for short-term funds to purchase expensive materials and cover inventory cost. All forms of lending, commercial and consumer, can be clunky and confusing to applicants, while lenders have a lot of boxes to check to ensure an applicant is eligible for a loan. It should be self-evident then that tracking Commercial Lending Key Performance Indicators (KPIs) are important to keeping lending services running smoothly and effectively – but property implementation of the right key performance indicators in commercial banks is more often overlooked than not.

What are Key Performance Indicators for Commercial Banks and Commercial Lending Operations?

Key Performance Indicators (KPIs) for Commercial Banks are defined as metrics, or quantitative and qualitative financial services business measurements, which are utilized by the commercial lending operations within a bank to monitor front office and back office commercial loan processes over a set period of time to compare against predetermined goals.

Measuring and benchmarking commercial banking operations key performance indicators has many benefits for financial institutions and banks of all sizes, including:

- Increasing the efficiency of commercial loan administration functions

- Increasing customer satisfaction with reduced commercial loan onboarding cycle times

- Creating more consistent commercial banking employee goals

- Reducing the amount of customer touch points through commercial lending operations

- Understanding the balance between loan types that are currently held by the bank

The above list only touches upon all the benefits of measuring commercial banking KPIs. Below we will go more in depth with four important commercial banking key performance indicators that should be measured by any financial institution dealing with business loans.

Key Performance Indicator for Commercial Banking #1: Commercial Loan Application Processing Cycle Time

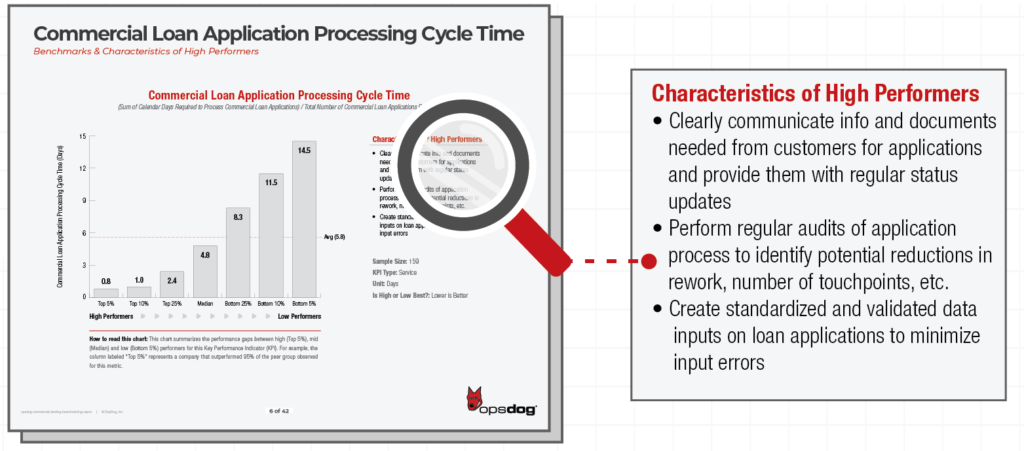

Long cycle times on commercial loan applications directly impact customer satisfaction. Businesses need to move fast and borrowers aren’t going to wait around for their application to be reviewed if other banks give them answers quicker and more efficiently.

Measuring Commercial Loan Application Processing Cycle Time will tell you the number of calendar days needed to fully process a commercial loan application from initial submittal to when underwriting review and approves or denies the application.

A lower value for this metric is best but in the case of a high number of days there are a few possible culprits:

- Confusing data input fields on loan applications that lead to errors and multiple revisions of paperwork

- Irregular audits of the commercial loan application process

- High levels of rework within the application process

Performing scheduled audits on the application process can be used to locate issues that are causing rework, confusing input fields, unclear documents, and other spots that could be improved upon.

Key Performance Indicator for Commercial Banking #2: Cost per Commercial Loan Origination

Commercial banks make money on the difference between what it costs them to produce a loan versus what the customer pays in interest and fees. A pillar of business operations is keeping costs low. So, keeping a close watch on this commercial banking KPI can expose low-value processes that are driving up costs, and help your team figure out how to improve margin on each commercial loan. Cost per Commercial Loan Origination should include labor costs, including benefits and bonuses, as well as overhead costs when calculating.

High origination costs can point to many problems within the process:

- Inefficient processing

- Multiple touch points and many customer follow-ups

- Understaffed or overstaffed support functions

- Poor performance from loan officers due to inconsistent training

Lowering cycle times for commercial loan origination can help lower costs as well as increase customer satisfaction. This measure aids in understanding operational performance and comparing your margin performance to peers in the industry.

Your customers are comparing you to your competitors, so let Opsdog help you do the same and align your commercial banking operations with industry benchmarks to ensure you stay ahead of the competition and gain new customers.

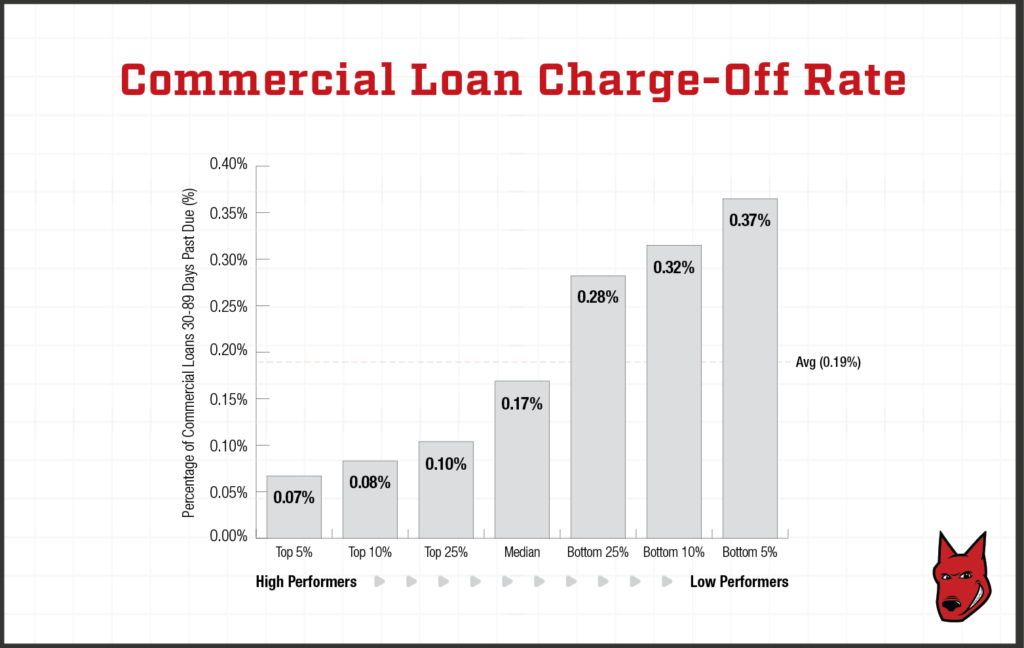

Key Performance Indicator for Commercial Banking #3: Commercial Loan Charge-Off Rate

This commercial banking KPI is closely related to risk in regard to underwriting methods in addition to being an indicator of possible losses caused by charge-offs. A charge-off is a delinquent loan that is unlikely to ever be collected by the organization. To calculate Commercial Loan Charge-Off Rate you take the remaining dollar amount of commercial loans that must be charged-off and divide it by the average dollar amount of total loans outstanding.

Below is an exert from Opsdog’s Commercial Lending KPI Benchmarking Report with 17 KPIs and Data Which Can Be Found for Sale Here

A lower percentage for this is best. A high value could mean that there are many high-risk loans in a commercial bank’s portfolio that they might never collect on. A high value can also point to numerous other issues, such as:

- Poorly defined processes in the collections department

- No predictive forecasts exist to target risky loans

- Procedures are not regularly reviewed so high-risk loans slip through the cracks

Performing poorly in this metric will hurt a bank’s overall market standing if not remedied. Loss reserves might need to be tapped to compensate for losses if too many loans are charged-off, negatively affected profitability.

Key Performance Indicator for Commercial Banking #4: Commercial Loans Outstanding per Commercial Loan Officer

Commercial loan officers are employees that are responsible for attracting new business, managing client relationships, and loan renewals for the bank or financial institution. This KPI measures total dollar amount of outstanding loans in relation to the number of commercial loan officers serving in the bank during a specific point in time.

When considering Commercial Loans Outstanding per Commercial Loan Officer, a higher value is best since this KPI deals with the productivity of customer facing employees. A low value can be contributed to a few different factors:

- Time-consuming or needlessly complex application processes

- Lull in commercial loan demands by customers

- High levels of rework

- Errors throughout applications caused by human error

- Poor training materials and a lack of oversight

Motivated commercial loan officers might spend time performing lead research to ensure they are reaching out to borrowers that fit the company’s “customer profiles” and are low-risk. Proper training and simplified application processes can help to boost the value of this KPI, boosting profitability and employee satisfaction.

Resources and Final Thoughts on Commercial Banking Key Performance Indicators

The above Key Performance Indicators are only a small sample of those available to track important processes to the Commercial Lending group. KPIs span many different areas, targeting quality, cost, productivity and more. Focusing on only one area may lead to deficits in other areas, so keeping a balanced spread of metrics is important to ensuring success in Commercial Lending processes.

Looking for a full list of Commercial Lending Key Performance Indicators? Download our ? Commercial Lending Benchmarking Report here.